Closing the Gap: A Strategic Blueprint for Women Navigating Britain's Retirement Wealth Inequality

Photo: SELF Magazine, CC BY 2.0, via Wikimedia Commons

Closing the Gap: A Strategic Blueprint for Women Navigating Britain's Retirement Wealth Inequality

The UK's gender pension gap is one of the most consequential and least discussed inequalities in British financial life. While the gender pay gap receives regular media attention and policy scrutiny, the retirement wealth differential — which is, by most measures, considerably larger — remains a subject that too few women encounter until it is too late to address it fully.

The statistics are stark. Research from the Pensions Policy Institute and successive government analyses consistently indicates that women in the United Kingdom retire with pension wealth approximately half that of men. For some demographic groups, particularly those who have taken extended career breaks or worked predominantly part-time, the shortfall is more severe still. Understanding why this gap exists is the essential first step towards closing it.

Photo: Pensions Policy Institute, via www.pensionspolicyinstitute.org.uk

Photo: Pensions Policy Institute, via www.pensionspolicyinstitute.org.uk

Photo: United Kingdom, via www.worldatlas.com

Photo: United Kingdom, via www.worldatlas.com

The Structural Architecture of Inequality

The gender pension gap is not the product of a single cause. It is the accumulated consequence of several interlocking structural features that compound against women across decades of working life.

The career break penalty. Women remain the primary caregivers in the overwhelming majority of British households. Maternity leave, extended parental absence, and career pauses to care for elderly relatives all create gaps in pension contribution records. For defined contribution schemes, every year of non-contribution is a year of lost employer matching, lost personal contributions, and — critically — lost compound growth on all of the above. A five-year career break in one's thirties does not simply cost five years of contributions; it costs the investment returns that those contributions would have generated over the following three decades.

Part-time work and the auto-enrolment threshold. Auto-enrolment has been transformative for British pension participation, but its design contains a significant flaw for part-time workers. Employees earning below £10,000 per year from a single employer are not automatically enrolled. Women, who constitute the majority of part-time workers in the UK, are disproportionately affected by this threshold. Many hold multiple part-time roles, none of which individually triggers auto-enrolment, leaving them entirely outside the workplace pension system despite being in active employment.

Salary disparity and contribution mechanics. Pension contributions are, for most workers, calculated as a percentage of salary. A persistent pay gap therefore translates directly into a persistent pension contribution gap. Even where contribution rates are identical between male and female employees, a lower base salary produces a lower absolute contribution — and a lower employer match — at every stage of a career.

Investment confidence and portfolio construction. Research suggests that women are, on average, more likely to hold pension savings in lower-risk, lower-return default funds for longer periods than their male counterparts. While this partly reflects rational risk preferences, it also reflects a confidence differential in engaging with investment decisions. Over a thirty-year accumulation period, the difference between a cautious default fund and an appropriately growth-oriented portfolio can represent a significant proportion of final retirement wealth.

The State Pension Foundation

Before addressing private pension strategy, it is worth ensuring that the state pension entitlement — which provides the foundational layer of retirement income for most British workers — is as strong as possible.

The full new State Pension currently requires 35 qualifying years of National Insurance contributions or credits. Women who have taken career breaks for childcare may have gaps in their NI record that reduce their eventual entitlement. However, two mechanisms exist to address this.

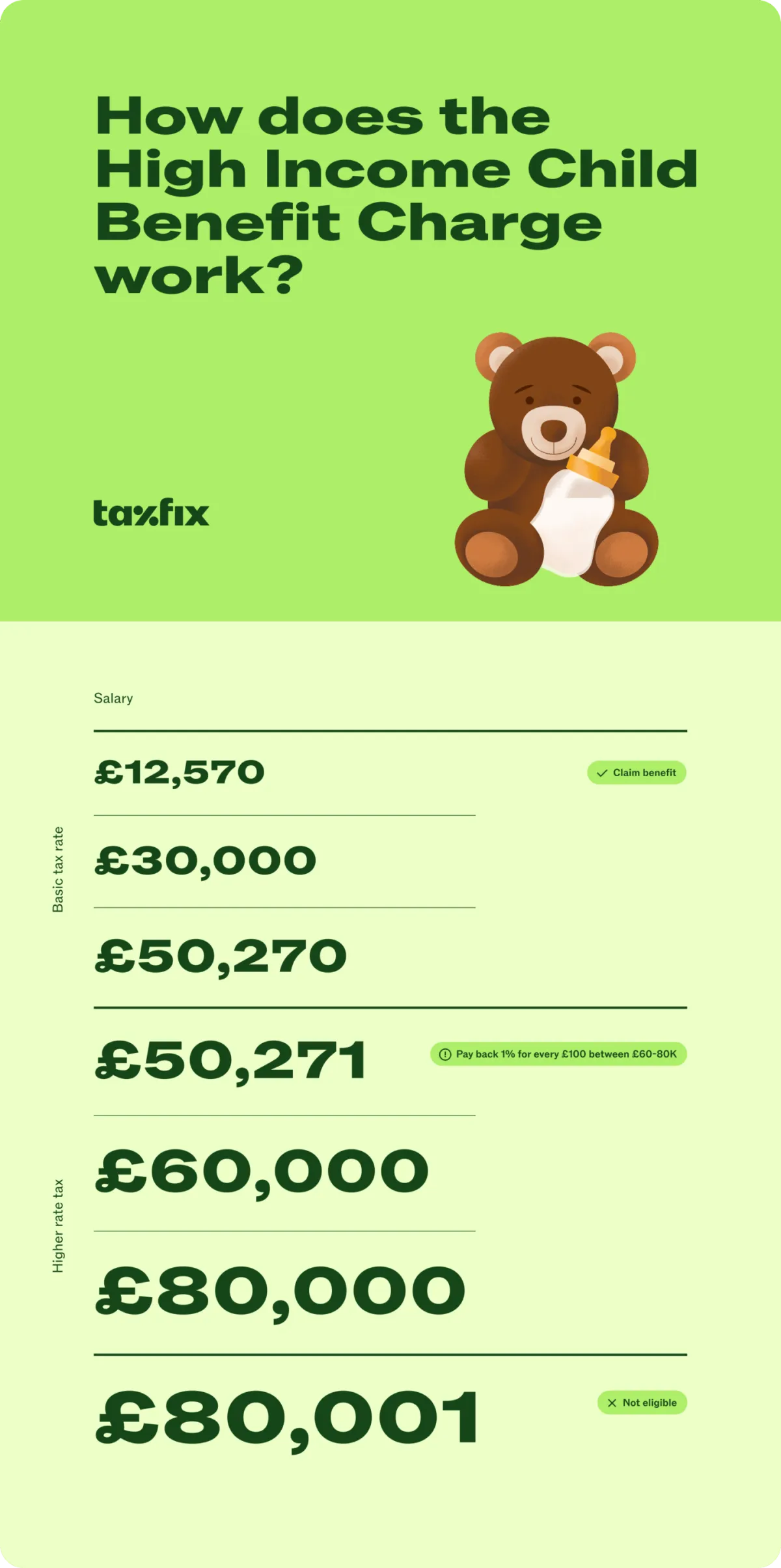

Child Benefit registration automatically confers NI credits for periods of childcare, provided the claim is made — yet a significant number of families have foregone Child Benefit in recent years due to the High Income Child Benefit Charge, inadvertently sacrificing the NI credits in the process. For those in this position, it may be worth revisiting whether the charge would actually apply and, if not, reinstating the claim.

Photo: Child Benefit, via taxfix.com

Photo: Child Benefit, via taxfix.com

For genuine NI gaps, voluntary Class 3 contributions can be used to fill missing years. The cost of purchasing a qualifying year is currently modest relative to the additional State Pension income it generates over a typical retirement. The government's online NI record checker provides a straightforward means of identifying gaps and modelling the cost-benefit of filling them.

Spousal Pension Contributions: An Underused Mechanism

For women who are not in paid employment, or whose earnings are below the annual allowance, a spouse or civil partner can make pension contributions on their behalf. Contributions of up to £2,880 per year can be made into a non-earner's pension, and the government will add basic rate tax relief, bringing the total annual contribution to £3,600.

This mechanism is straightforward, tax-efficient, and frequently overlooked. For a couple where one partner has taken a career break, directing a portion of the working partner's income into the non-working partner's pension — rather than concentrating all retirement saving in a single arrangement — can produce a more balanced outcome at retirement and, in certain circumstances, a more tax-efficient income distribution in later life.

The Lifetime ISA as a Complementary Vehicle

For women under the age of 40 who are building retirement savings, the Lifetime ISA warrants serious consideration as a complement to pension provision. The government adds a 25 per cent bonus on contributions of up to £4,000 per year, producing a maximum annual bonus of £1,000. Over a twenty-year accumulation period, the compounded effect of this bonus is substantial.

The Lifetime ISA does carry restrictions — withdrawals before age 60 for non-property purchase purposes attract a penalty — but as a dedicated retirement savings vehicle for those who may also be saving for a first property, it offers a degree of flexibility that a pension cannot.

Practical Steps at Every Career Stage

The appropriate response to the gender pension gap varies considerably depending on where a woman currently sits in her working life.

In your twenties and early thirties: The most powerful action available is simply to begin contributing as early as possible and to ensure that contributions are invested in an age-appropriate, growth-oriented portfolio rather than a default fund selected for its caution. The compounding advantage of early investment is asymmetric — years gained at the beginning of an accumulation period are worth considerably more than equivalent years added at the end.

During a career break: Maintain pension contributions if at all possible, even at a reduced level. Register for Child Benefit to protect NI credits. Consider whether spousal contributions into your own pension are achievable. Review your NI record annually.

In your forties and fifties: This is the period in which the gap becomes most visible and, for many women, most alarming. It is also the period in which higher earnings and lower family costs may create genuine capacity to accelerate contributions. Annual allowance carry-forward provisions allow unused pension allowances from the previous three tax years to be utilised, potentially enabling a significant one-time contribution boost.

Approaching retirement: Sequence of returns risk — the danger that poor market performance in the years immediately before and after retirement permanently impairs the portfolio — is a specific concern for those with lower pension balances. A financial planner can model decumulation strategies, including phased drawdown and annuity combinations, that maximise income sustainability for the available fund.

A Gap That Can Be Narrowed

The structural causes of Britain's gender pension gap will not be resolved quickly. Policy changes to auto-enrolment thresholds, employer contribution requirements, and childcare provision will take years to feed through into improved retirement outcomes. But the individual strategies outlined above are available now, to women at every income level and career stage.

The retirement wealth gap is, to a meaningful degree, a planning gap — one that can be significantly narrowed by those who engage with it deliberately and early enough. The financial future available to British women need not be determined by the structural disadvantages they have inherited.