Generation X's Retirement Reckoning: The Pension Gap That Could Define a Generation's Financial Future

Photo: Basher Eyre, CC BY-SA 2.0, via Wikimedia Commons

Generation X's Retirement Reckoning: The Pension Gap That Could Define a Generation's Financial Future

There is a quiet financial crisis unfolding in Britain's suburbs, semi-detached houses, and corporate open-plan offices. It does not appear on the front pages of newspapers, nor does it feature prominently in government financial inclusion campaigns. Yet for the cohort of Britons currently aged between 42 and 58, the arithmetic of retirement is producing some deeply uncomfortable conclusions.

Generation X — broadly defined as those born between 1965 and 1980 — occupies a uniquely unfortunate position in the history of British retirement provision. They arrived in the workforce too late to accumulate meaningful years within the generous defined benefit pension schemes that secured comfortable retirements for their parents. Yet they came of age financially before the smartphone-enabled, low-cost investment platforms that have encouraged younger cohorts to engage with their money from their twenties. The result is a generation caught between two eras, benefiting fully from neither.

The Numbers Behind the Shortfall

The Pensions Policy Institute estimates that the average Generation X worker will retire with a pension pot of approximately £105,000 — a figure that sounds substantial until it is placed alongside the income it can realistically generate. Using current annuity rates, that sum translates to a guaranteed income of roughly £5,500 per annum. Combined with the full new State Pension of £11,502 for the 2024/25 tax year, the total projected retirement income for a typical Gen X individual sits at approximately £17,000 annually.

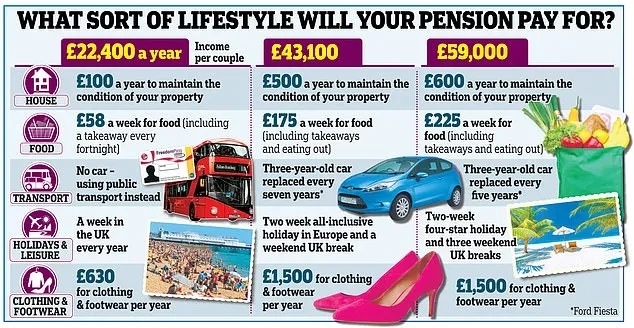

The Retirement Living Standards research published by the Pensions and Lifetime Savings Association places the cost of a 'moderate' retirement lifestyle — one that includes a fortnight's holiday abroad, regular social activities, and reasonable home maintenance — at £31,300 per year for a single person. The gap between projected income and that moderate standard is therefore approaching £14,000 annually. Over a 20-year retirement, that shortfall compounds into a staggering deficit of real purchasing power.

Photo: Pensions and Lifetime Savings Association, via i.dailymail.co.uk

Photo: Pensions and Lifetime Savings Association, via i.dailymail.co.uk

For those hoping to sustain what the same research terms a 'comfortable' retirement — incorporating greater leisure, a newer car, and some financial flexibility — the annual requirement rises to £43,100, widening the shortfall still further.

Why Generation X Fell Through the Cracks

Understanding how this situation arose is essential before addressing how it might be remedied. Three structural factors conspired against this cohort simultaneously.

First, the mass closure of defined benefit schemes during the 1990s and early 2000s removed the most reliable mechanism for building retirement income precisely as many Gen X workers were entering their peak earning years. Those who had accumulated a handful of years within such schemes were often transferred into defined contribution arrangements with far less certainty about eventual outcomes.

Second, auto-enrolment — the policy that has dramatically improved pension participation among younger workers — was not introduced until 2012, arriving too late to instil savings habits during the formative early career years that carry the greatest compound growth potential. Many Gen X workers spent their twenties and early thirties with no workplace pension provision whatsoever.

Third, the financial pressures of midlife — mortgage repayments, childcare costs, and in some cases supporting ageing parents — have compressed the disposable income available for discretionary pension contributions during the very years when those contributions would carry the greatest long-term value.

The Compounding Penalty of Delayed Action

The mathematics of compounding means that delayed pension contributions are not merely postponed — they are fundamentally diminished in their eventual impact. A £500 monthly contribution begun at age 25 and growing at 6% annually will accumulate to approximately £995,000 by age 65. The same contribution begun at age 45 produces only £232,000 over the same rate of return. This is not a marginal difference; it represents a £763,000 penalty for a 20-year delay.

For Generation X, this reality is not reversible. What it does mean, however, is that the remaining working years carry exceptional strategic importance. Every year of inaction between now and retirement amplifies the eventual shortfall.

Practical Strategies for Closing the Gap

Pension consolidation as a foundation. Many Gen X individuals hold multiple small pension pots accumulated through a series of employers, each carrying its own annual management charges and administrative complexity. Consolidating these into a single Self-Invested Personal Pension (SIPP) or a well-governed workplace scheme can reduce costs, simplify monitoring, and in some cases unlock access to a broader range of investment options. Before consolidating, it is essential to verify that no valuable guaranteed benefits — such as safeguarded defined benefit rights — are being surrendered in the process.

Maximising employer matching before all else. Employer pension matching represents an immediate, guaranteed return on contributions that no investment vehicle can replicate. Yet research consistently shows that a significant proportion of British employees contribute only the minimum required to trigger auto-enrolment, leaving substantial employer matching unclaimed. Increasing personal contributions to the maximum matched level should be the first priority for any Gen X worker reviewing their retirement strategy.

Utilising carry forward allowances. Those with the capacity to make larger lump-sum contributions should investigate the pension carry forward rules, which allow unused Annual Allowance from the previous three tax years to be deployed in the current year. For higher earners, this can enable pension contributions substantially in excess of the standard £60,000 Annual Allowance, accelerating pot accumulation considerably.

ISA wrappers as complementary vehicles. The £20,000 annual ISA allowance provides a tax-efficient savings vehicle that, while lacking the upfront tax relief of pension contributions, offers complete flexibility on withdrawal timing and no requirement to purchase an annuity or draw down in a prescribed manner. For Gen X investors approaching retirement, a blend of pension and ISA accumulation can provide both tax efficiency in the accumulation phase and sequencing flexibility in the drawdown phase.

Revisiting investment risk appetite. Many Gen X pension holders remain in default funds that were selected by their employer and have never been reviewed. These funds often adopt a 'lifestyling' approach that progressively de-risks the portfolio as retirement approaches — a strategy designed for those purchasing an annuity, but potentially inappropriate for those planning a flexible drawdown retirement spanning two or three decades. A review of fund selection, ideally with professional guidance, may reveal opportunities to capture greater long-term growth without inappropriate risk exposure.

The Cost of Inaction

The pension shortfall facing Generation X is not a fixed, inevitable outcome. It is the cumulative product of structural disadvantage, financial pressure, and — critically — inaction at moments when action remained meaningful. With between 7 and 23 working years remaining for most of this cohort, the capacity to materially alter retirement outcomes still exists.

What it requires is an honest appraisal of the current position, a willingness to prioritise retirement provision even against competing financial demands, and in many cases, access to professional financial planning that can translate the complexity of pension rules, allowances, and investment options into a coherent personal strategy.

At Asset Grove, we work with clients across all life stages to build retirement strategies that are grounded in current realities rather than optimistic assumptions. For Generation X, the most valuable financial decision of 2025 may simply be to look clearly at the numbers — and then act.